Peloton: Next-Gen Social Network

Social enablement will drive the next phase of OEM competition

“You have a new follower on Peloton”

The last time that I opened notification e-mails with such interest? College.

While the subject line has become mundane, the strategy continues to fascinate. So, too, do the competitive implications that follow from Peloton’s decision to build a proprietary social graph.

This strategy—quickly replicated by Peloton’s competitors—points to the next phase of original equipment manufacturer (“OEM”) competition, a phase defined not by incremental hardware improvements but by greater user-to-user connectivity.

Overview

The following explains how OEM competition has evolved over the past decade, outlines why social enablement will shift the scope of future competition, and identifies strategic objectives that OEMs should prioritize to achieve commercial success.

An extended discussion of these points follows, with key takeaways summarized in the bullets below.

Key takeaways:

During the last decade, new entrants such as Peloton and Hydrow upended the hardware industry. In response, traditional OEMs invested in digital capabilities while digitally-native OEMs pursued greater user-to-user connectivity.

User-to-user connectivity unlocks ecosystem value, a dynamic value proposition that supplements hardware’s standalone value. Of note, ecosystem value benefits from demand-side increasing returns, or “network effects”.

As socially-enabled OEMs scale up, ecosystem value will deliver a greater share of their all-in value propositions. As a result, the hardware market will begin to see greater ecosystem, or network-driven, competition.

Network-driven competition often leads to winner-take-all commercial outcomes. To best position themselves as the ultimate “winner,” OEMs should prioritize strategic objectives such as 1) social enablement, 2) relative scale gains, and 3) ecosystem signaling.

OEM Competition: Past to Present

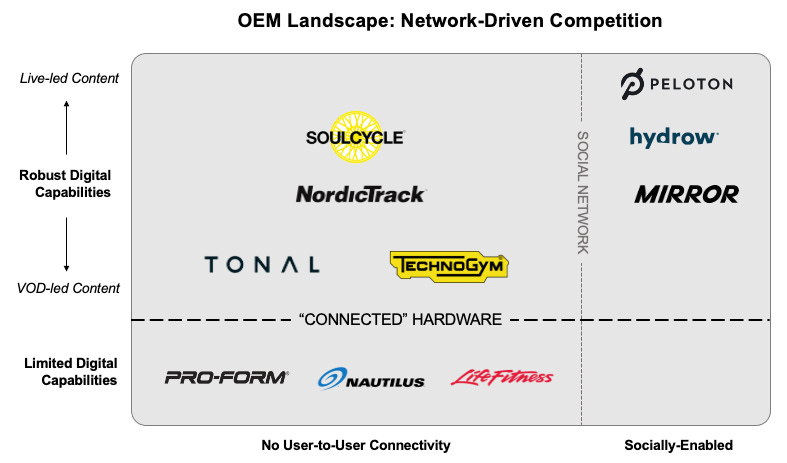

For much of their histories, hardware manufacturers differentiated their product lineups primarily through tactile features. These features, such as form factor and material finishes, had a direct impact on the user experience and ultimately informed consumers’ quality assessments. For example, TechnoGym equipment often delivered experiences superior to those offered by lower-cost manufacturers such as Pro-Form and Life Fitness. A consistently better user experience—made possible through significant investments in the product development cycle—enabled TechnoGym to develop a reputation for quality, command premium pricing, and carve out an economically-viable market niche. This commercial relationship, between equipment’s all-in production costs and its perceived quality, defined the early decades of OEM competition and underpinned a competitive equilibrium that saw multiple manufacturers—across the cost-quality continuum—achieve commercial success.

Digitally-native manufacturers such as Peloton and Hydrow upended this market equilibrium. These new entrants offered premium finishes and robust digital capabilities; they integrated hardware and software to deliver qualitatively better user experiences. And as consumers became more familiar with these integrated offerings—which boasted live classes, dynamic content libraries, and content interactivity—digital considerations increasingly factored into consumers’ all-in quality assessments. Whereas equipment “quality,” had historically been defined according to analog considerations, it quickly became synonymous with an integrated—and digitally-robust—user experience.

A more expansive definition of hardware quality precipitated a shift in the competitive landscape. Traditional OEMs such as TechnoGym and NordicTrack, whose equipment offered relatively limited—if any—digital capabilities, saw their competitive positions weaken. In contrast, digitally-native OEMs, whose integrated lineups often competed at price points comparable to those of their analog competitors, benefited from the incremental value that customers ascribed to robust digital offerings. In short, changing consumer preferences bifurcated the hardware market and led to divergent outcomes on either side of the digital divide.

Following this market shift, traditional manufacturers have sought to close the perceived quality gap with their integrated, upstart rivals. For example, companies such as NordicTrack have invested in new, digitally-capable hardware lineups. These new lineups, now in market, boast digital features comparable to those originally introduced by companies such as Peloton. As evidence of its success in achieving feature parity, NordicTrack has even found itself on the receiving end of a patent infringement lawsuit. In aggregate, these investments have helped traditional OEMs bridge the digital divide, deliver relatively greater value to prospective consumers, and improve their strategic positioning. Thus, both traditional and digitally-native OEMs can now tout integrated (or “connected”) hardware lineups.

OEMs: Next-Gen Social Networks

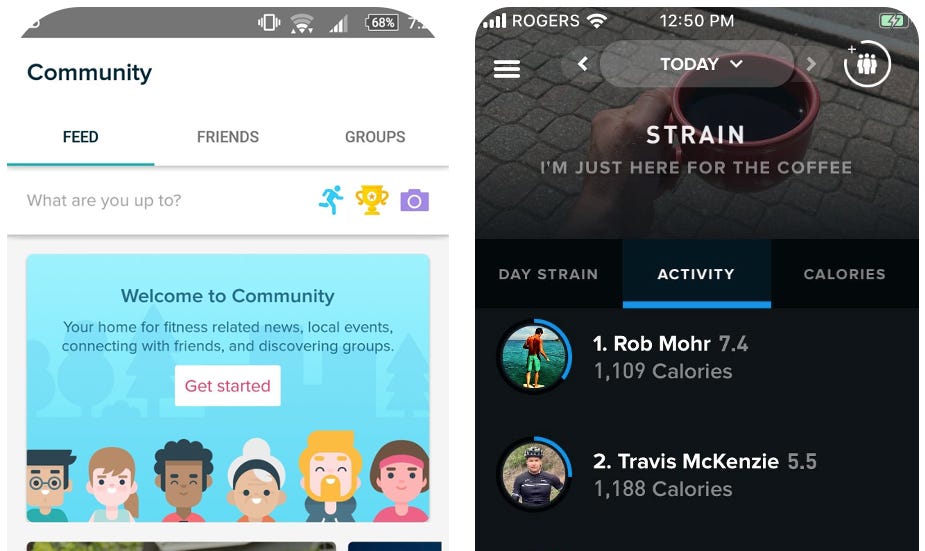

As integrated offerings have become an industry standard, digitally-native OEMs have sought to maintain their innovation leads. During the past year, OEMs have pursued this strategic objective by investing in user-to-user connectivity. For example, Peloton expanded its social offerings by introducing profile hashtags and Sessions, synchronized exercise experiences available to those with Peloton-branded hardware. At the other end of the spectrum, Hydrow and Mirror—which did not yet offer social capabilities—shipped “Find & Follow” and “Friend” features, respectively.

Unlike previous digital investments, social features unlock a new source of consumer value, one generated by an OEM’s install base—its wider ecosystem—rather than the hardware itself. Said differently, social enablement effectively transforms OEMs’ install bases into nascent social networks, whose cost of entry is the hardware itself.

As with most networks, hardware-centric networks benefit from demand-side increasing returns (DSIR), or network effects. DSIR is a phenomenon in which a network’s value increases to all participants as the size of the network grows. An oft-cited example is the telephone service, whose overall utility increases to all participants as more people purchase telephones and become reachable through the service. When applied to the hardware market, DSIR implies that the value of a manufacturer's hardware ecosystem increases as its install base grows. Equipment sales translate to more potential connections and more opportunities to enjoy shared experiences. In other words, social features unlock a dynamic source of value that can supplement hardware’s standalone, or equipment-centric, value proposition.

As socially-enabled OEMs expand their footprints, ecosystems will contribute a growing share of the all-in value offered to consumers. While equipment-centric value will continue to drive marginal purchases in the short run, this relatively static value proposition will increasingly give way to ecosystem considerations, particularly as more OEMs unlock social features; build around user-to-user connections; and scale up their install bases. Such incremental investments should, over time, accelerate ecosystem value accretion and—as a consequence—lead to relatively more ecosystem-driven purchases.

By way of example, if forced to choose between purchasing an exercise bike from Bowflex or Peloton, many consumers would opt for the former. Bowflex’s lower price point and its relatively comparable feature set (i.e., its equipment-centric value) suggest a better deal, even after accounting for ecosystem value. Yet, were these same consumers to revisit their purchase decisions at a later date, then their preferences might change. If during the interim period, their family and friends either joined or expressed the desire to join the Peloton ecosystem, then these same buyers might ascribe relatively greater value to Peloton’s offering. And, if sufficiently large, this incremental value—actual or expected—could ultimately tip the purchase decision from Bowflex to Peloton.

If the hardware market’s trajectory follows that of other networked markets, then greater ecosystem competition can lead to lopsided commercial outcomes. As previously discussed, consumer expectations and purchase decisions can become mutually reinforcing, particularly when ecosystem value drives marginal purchase decisions. Forward-looking customers will align themselves with the hardware ecosystems that deliver—or are expected to deliver—the greatest all-in value. If these customers have similar expectations and ultimately join the same ecosystem, then they will increase the value of said network and will incentivize yet more customers to make the same purchase decision.

In aggregate, these behaviors can contribute to winner-take-all outcomes in which the most attractive ecosystem, or perceived “winner,” realizes disproportionate commercial upside vis-á-vis those with less attractive prospects. We see early evidence of this winner-take-all dynamic in the market today. During the past year, Peloton has seen robust growth even as competitors’ offerings have seemingly achieved feature parity. And at the opposite end of the spectrum, SoulCycle’s At-Home Bike has failed to gain significant traction despite the company’s strong brand equity and loyal in-person following.

Winning A Networked Future

As ecosystem, or network-driven, competition takes hold, OEMs will need to pursue strategies that best-position them to become the hardware market’s actual, or perceived, “winner”.

For category leaders such as Peloton and Mirror, these strategies should seek to accelerate timelines for tipping categories in their favor. For relative laggards such as SoulCycle; NordicTrack; and Bowflex, these strategies should accelerate install base growth and create opportunities for leapfrogging category leaders. Regardless of their current market positions, all manufacturers should ensure that their strategies deliver on three key objectives: 1) social enablement, 2) relative scale gains, and 3) ecosystem positioning.

An in-depth discussion of each objective follows.

Social Enablement

OEMs must invest in social features to unlock network effects across their install bases. Absent user-to-user connectivity, OEMs will see their competitive positions erode as ecosystem value drives a larger share of purchase decisions.

When applied, this guidance suggests that manufacturers which have not yet unlocked network effects should either build social features in-house or partner with an existing social graph. The decision to build or partner should be determined based on an OEM’s technical capabilities.

Build: Digitally-savvy OEMs such as Tonal, which already maintain standalone applications, may be better-positioned to build social capabilities into their existing digital channels. Following Hydrow’s lead, these companies can introduce basic features such as “Follow” or “Friend” to build out their social graphs. Afterwards, OEMs can build incremental experiences on top of these nascent social graphs to enhance the value of user-to-user connectivity. The build approach may also be preferable for companies with strong digital know-how and significant brand equity. For example, social features could dramatically increase the attractiveness of SoulCycle/Variis, particularly among brand loyalists who want to replicate their in-person networks in a digital environment.

Partner: In contrast, traditional OEMs such as NordicTrack and Bowflex, whose digital capabilities trail those of their digitally-native counterparts, may find it more efficient to outsource social enablement. These OEMs should consider partnering with third-parties that offer access to robust, easily-accessible social graphs. For example, by leveraging Fitbit, Whoop, or Facebook’s** social graphs, these OEMs could quickly transform their most strategic resources—their extensive install bases—into market-leading networks.

Fitbit and Whoop have developed in-app communities.

**Disclosure: I work at Facebook.

Relative Scale Gains

In network-driven markets, scale confers a source of competitive advantage. Given this strategic benefit, socially-enabled OEMs should prioritize go-to-market efforts that increase conversion rates and accelerate install base growth. OEMs can accelerate install base growth through multiple initiatives, including pricing and interoperability.

Pricing: Price, or the cost of entry, has a disproportionate impact on consumers’ purchasing decisions. All else equal, lower-priced hardware attracts customers and higher-priced hardware deters customers. Given this heuristic, OEMs can accelerate install base growth by reducing upfront commitment costs. We see evidence of this strategy across the hardware industry. Peloton and SoulCycle both offer financing options that transform eye-watering list prices into manageable monthly payments. Other examples include NordicTrack’s decision to bundle its iFit digital service, which retails for hundreds of dollars, with new equipment purchases.

Interoperability: By making their hardware compatible with third-party products and services, manufacturers can increase the relative attractiveness of their ecosystems. For example, both Mirror and Peloton integrate with the Apple Watch/iOS ecosystem. This compatibility increases the value of Mirror and Peloton to all Apple Watch owners and, on the margin, may incline prospective customers to purchase from these manufacturers. In fact, recent marketing efforts suggest that OEMs subscribe to this commercial logic. Peloton prominently featured the Apple Watch integration in its Bike+ announcement. And per 9to5 Mac, this integration eliminated a distinct source of consumer friction, namely the need to “purchase a second [heart rate monitor]” for Peloton workouts.

Ecosystem Positioning

As discussed, consumer expectations can inform perceived ecosystem value. Ecosystems that appear healthier will offer relatively greater expected value while those that appear weaker will offer less expected value. And because expected ecosystem value factors into purchasing decisions, OEMs have strong incentives to position their hardware networks as either the inevitable winner, or one that will remain viable throughout the duration of the equipment’s useful life.

OEMs can signal ecosystem health and longevity in a number of ways, including strategic partnerships and public commitments. For example, Peloton’s partnership with Beyoncé sent a strong signal to consumers about the company’s prospects. The partnership suggested that Beyoncé viewed the company as a “winner,” as an ecosystem worthy of her time and talents. Such an endorsement provides a strong signal to the market and, as a consequence, will likely drive incremental equipment sales.

For OEMs with ambiguous long-term prospects, similar endorsements or partnerships could shift consumer perceptions and drive incremental ecosystem buy-in. For example, SoulCycle could leverage Equinox’s roster of talent, brands, and corporate relationships to signal the company’s long-term commitment to its at-home offering. Alternatively, if SoulCycle has recently experienced significant volume growth, then the company should consider making a public announcement to give SoulCycle-inclined buyers yet another reason to join the ecosystem.

Wrap

Just as digital innovation disrupted the hardware market, so too will user-to-user connectivity. This disruption, combined with the possibility of winner-take-all outcomes, increases the competitive stakes for all market participants.

That said, manufacturers still have sufficient time—and ample opportunities—to execute against strategies that will improve their competitive positions and set them up for long-term success. OEMs that lean into social enablement, prioritize install base growth, and position their ecosystems effectively will increase the likelihood that they emerge as the market’s ultimate winner.